Insights from the Dutch MAP Annual Report 2025 and the EU Tax Omnibus Proposal

Recent developments in international tax dispute resolution

Several recent developments illustrate the continued focus on improving international tax dispute prevention and resolution mechanisms. In this context, the publication of the Dutch MAP team's 2025 Annual Report and the European Commission's Tax Omnibus Proposal are particularly noteworthy. The Annual Report provides insights into the use and effectiveness of mutual agreement procedures (MAPs) in the Netherlands, while the Tax Omnibus Proposal includes amendments to the EU Dispute Resolution Mechanism Directive aimed at further enhancing cross-border tax dispute resolution within the European Union.

Dutch MAP Annual Report 2025

As transfer pricing audits continue to increase globally, multinational groups are placing greater emphasis on tax certainty and effective dispute resolution mechanisms. The recently published Mutual Agreement Procedures (MAP) Annual Report 2025 provides insights into how the Netherlands continues to support the resolution of international tax disputes and the elimination of double taxation.

With tax authorities around the world investing further in transfer pricing audit capabilities, multinational groups face an increased likelihood of detailed examinations of their transfer pricing policies, particularly in areas involving intangibles, financing arrangements and business restructurings. The continued use of Advance Pricing Agreements (APAs), bilateral APAs (BAPAs) and multilateral APAs (MAPAs) reflects the growing demand among taxpayers for greater certainty in this environment.

For many taxpayers, a proactive BAPA or MAPA strategy can help prevent future disputes. When disputes do arise, MAP remains an important mechanism for eliminating double taxation. According to the annual report, 97% of MAP cases in the Netherlands were successfully resolved.

A factor that may contribute to this outcome is the availability of pre-filing meetings. Before formally submitting a MAP, BAPA or MAPA request, taxpayers may engage in an informal and non-binding discussion with the Dutch tax authorities. Such discussions can provide greater clarity on procedural aspects and help assess whether a request is likely to be suitable and effective in the relevant circumstances.

The report also notes that, in a MAP context, taxpayers may request mitigation of tax interest or collection interest charged in the Netherlands. This possibility is generally not available in BAPA or MAPA cases.

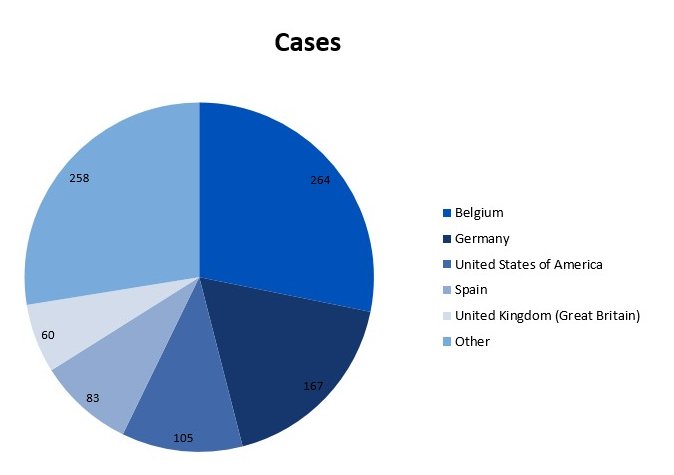

This graph shows the five jurisdictions with which the Netherlands had the highest number of MAP cases in 2025.

European Commission Tax Omnibus Proposal

A second noteworthy development is the Tax Omnibus Proposal published by the European Commission on 24 June 2026. The proposal includes amendments to the EU Dispute Resolution Mechanism (DRM) Directive, also known as the Arbitration Directive. The Directive establishes a framework for resolving disputes concerning the interpretation and application of tax treaties, with the aim of eliminating double taxation affecting both businesses and individuals.

For a practical discussion of the current DRM framework, reference can be made to KPMG Meijburg & Co's publication on key considerations regarding the EU Arbitration Directive.

The proposed amendments focus on improving procedural clarity, accessibility and efficiency. Key proposals include:

- clarification of the scope of the Directive;

- simplification of the complaint procedure;

- clearer rejection grounds combined with additional taxpayer safeguards, including a 30-day remedy period;

- earlier notification requirements where competent authorities fail to reach agreement;

- an extension of the scope to include admissibility disputes; and

- simplified filing procedures for SMEs and individuals.

Further details on the proposal can be found in the recent publication of KPMG's EU Tax Centre.

The proposed amendments are intended to enhance the effectiveness and accessibility of the EU dispute resolution framework. The extent to which these objectives are achieved will depend on the implementation and practical application of the revised rules by EU Member States. The European Commission has indicated that it will monitor the functioning of the framework and conduct a formal evaluation in 2030.

Looking ahead

Over the past decade, international efforts to address double taxation have increasingly focused not only on prevention, but also on the availability of effective dispute resolution mechanisms. MAPs, APAs and arbitration procedures play an important role in providing taxpayers with certainty and facilitating the resolution of cross-border tax disputes.

The Dutch MAP Annual Report 2025 highlights the continued relevance of MAPs, APAs and pre-filing meetings as tools for managing international tax risk and resolving disputes. At the same time, the European Commission's proposed amendments to the DRM Directive demonstrate an ongoing commitment to improving access to dispute resolution within the European Union.

Multinational groups may therefore wish to consider dispute prevention and dispute resolution mechanisms as part of their broader tax risk management strategy. Assessing available options at an early stage can help reduce uncertainty and improve the management of potential cross-border tax controversies.

Want to know more?

Our Tax Controversy & Litigation team can assist taxpayers in evaluating and implementing an appropriate strategy in the context of international tax disputes, in close cooperation with KPMG's global network of tax controversy professionals.